Understanding What A Second Mortgage Is For Florida Homeowners

If you don’t already know, Florida is known for its active real estate market, with many people purchasing homes and properties for a better quality of life and investments. Now, understanding home finance in Florida is crucial as it helps homeowners to plan and budget their finances effectively. That said, it’s important to understand what a second mortgage is and how it can help access home equity and financing needs. As always, Florida homeowners should consult financial experts and do thorough research before making any decisions related to home finance. Let’s get right into it and go over the types of second mortgages, what a second mortgage is, and how a second mortgage works.

How A Second Mortgage Works

One of the common ways homeowners can access funds or equity in their homes is through a second mortgage. A second mortgage is a loan taken out against the equity in the already mortgaged home. It is typically used for home improvements, renovations, or debt consolidation. Second mortgages can be a great option for homeowners with equity in their homes and need access to funds. Some may even consider a second mortgage to use as capital for a fix and flip house in Florida.

Homeowners in Florida may access funds or equity in their homes through a second mortgage. Two categories of second mortgages are home equity loans and home equity lines of credit, also known as a HELOC.

Understanding What A Second Mortgage Is: Home Equity Loan or Lump-Sum Loan

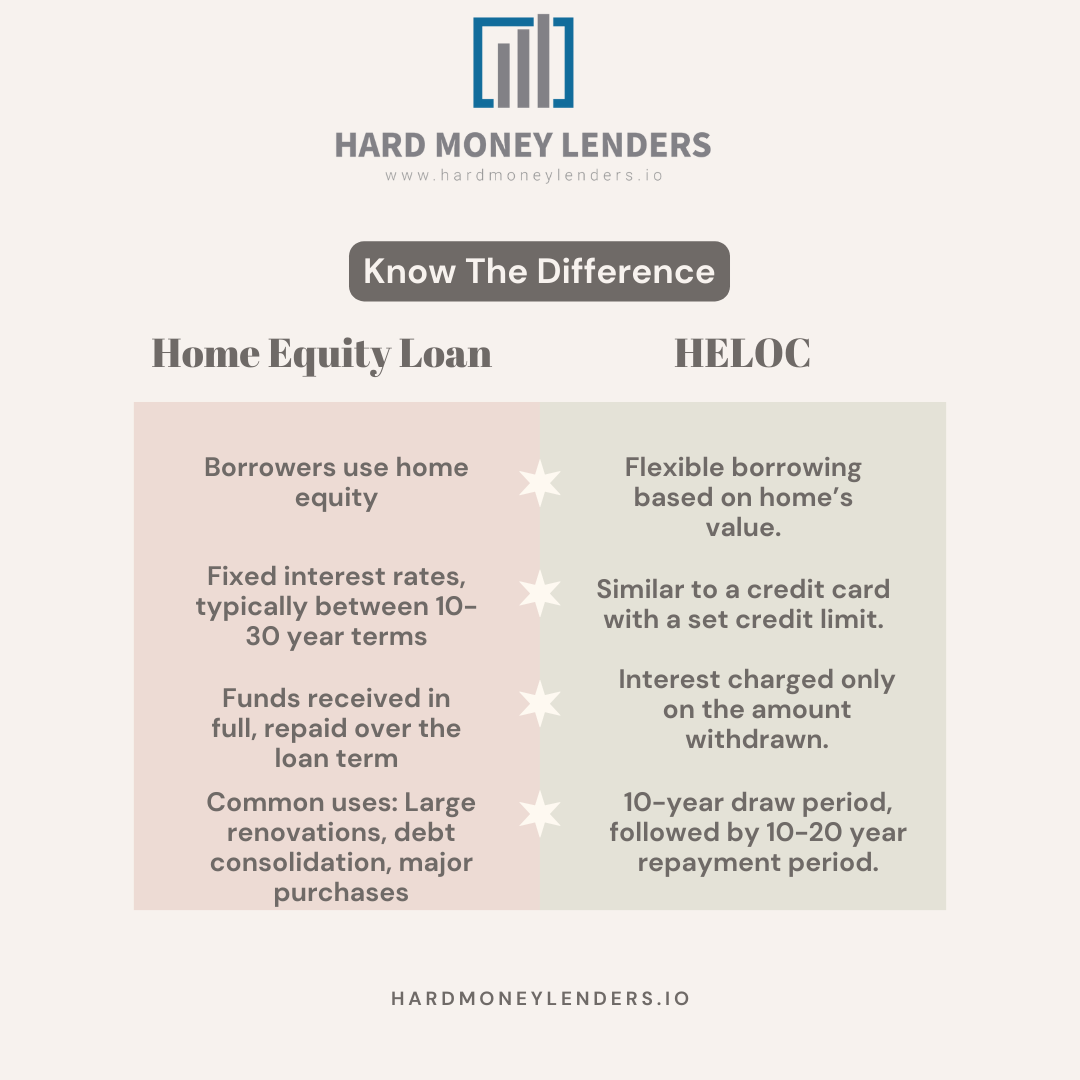

Home equity loan, also known as a lump-sum loan, enables homeowners to borrow money using the equity in their homes. Equity is defined as the discrepancy between the current market value of a home and the remaining mortgage debt. Home equity loans usually have a fixed interest rate and a term of 10 to 30 years. The borrower receives the loan amount in full and repays it with interest over the term of the loan.

If you don’t know already, home equity loans are typically used for large home renovations, debt consolidation, or major purchases.

Understanding home equity line of credit

A HELOC is a flexible financing option where homeowners can borrow money based on the home’s value.

Now, A HELOC is similar to a credit card, as the borrower is granted a specific credit limit, and the borrower can draw funds as needed. The interest rate for a HELOC may be variable and tied to the prime rate, and the borrower is only charged interest on the amount withdrawn. HELOCs usually have a draw period of 10 years, during which the borrower can use the funds, which is typically followed by a repayment period of 10 to 20 years.

As always, homeowners in Florida should consult with financial experts and research their options thoroughly before deciding which type of second mortgage is right for them. It is important to understand the terms and conditions, fees, and interest rates associated with second mortgages to make informed decisions about their home finance.

Second Mortgages Are Secured By The Borrower’s Home

Both types of second mortgages are secured by the borrower’s home and would be considered as a lien against the property. Interest rates on second mortgages may be higher than those on first mortgages, as there is an increased risk to the lender due to the lower priority of the second loan in the event of default.

When a borrower applies for a second mortgage, they will need to go through the same process of providing financial documentation, credit checks, and home appraisals as they did with their first mortgage. Once approved, the borrower will receive the funds in full for a home equity loan or can draw from the HELOC as needed.

Reasons to Get a Second Mortgage

Consolidating debt

One reason to get a second mortgage is to consolidate debt. By using a home equity loan or HELOC, borrowers can pay off high-interest debts such as credit cards or personal loans. This can simplify debt repayment and potentially lower overall interest rates.

Home improvements

Another reason to access a second mortgage is to make home improvements. Borrowers can use the funds to make upgrades or repairs to their homes, which can increase property value and potentially reduce overall maintenance costs. However, borrowers should carefully consider the cost of the improvements relative to the potential increase in value.

Benefits of Second Mortgage

A second mortgage allows homeowners to access the equity in their homes. Both types of second mortgages (HELOC and home equity loan) are secured by the borrower’s home and are considered liens against the property.

Lower interest rates

One benefit of a second mortgage is that the interest rates may be lower than those on other types of loans, such as credit cards or personal loans. This is because the loan is secured by the borrower’s home, which reduces the risk to the lender. However, interest rates on second mortgages may be higher than those on first mortgages due to the increased risk to the lender.

Tax-deductible interest

One advantage of obtaining a second mortgage is that the interest paid on it can potentially be deducted from taxes. Homeowners may be able to deduct the interest paid on a home equity loan or HELOC from their taxes if they use the funds to improve their homes. However, it is important to consult with a tax professional to understand the specific requirements and limitations.

No need to refinance your current mortgage

A third benefit of a second mortgage is that homeowners do not need to refinance their current mortgage to access the equity in their homes. This makes it a more convenient option for homeowners who do not want to go through the refinancing process.

It is important to carefully consider the terms and conditions, fees, and interest rates of a second mortgage before taking one out. Homeowners should consult with financial experts and thoroughly research their options to determine if a second mortgage is the best choice for them.

How A Second Mortgage Works: Risks and Considerations

While a second mortgage can provide homeowners with access to the equity in their homes, there are also risks and considerations to keep in mind.

Your property is collateral

One important thing to consider is that a second mortgage is secured by your home. This means that if you are unable to make your payments, the lender can foreclose on your property. Before taking out a second mortgage, it’s important to carefully consider your ability to make payments and ensure that you are not putting your home at risk.

Higher debt-to-equity ratio

Taking out a second mortgage can also impact your debt-to-equity ratio, which is the amount of debt you have compared to the value of your home. If you already have a high amount of debt or a low amount of equity in your home, taking out a second mortgage can further increase your ratio and make it harder to obtain credit in the future.

Possible foreclosure if unable to pay

If you are unable to make your payments on a second mortgage, your lender can foreclose on your property. This can have serious consequences, including the loss of your home and damage to your credit score. Before taking out a second mortgage, it’s important to carefully consider your ability to make payments and ensure that you have a solid plan for paying off the loan.

Overall, a second mortgage can be a useful tool for accessing the equity in your home, but it’s important to carefully consider the risks and ensure that you are making a smart financial choice. Consult with financial experts, thoroughly research your options, and make sure that a second mortgage is the best choice for your unique financial situation.

How to Qualify for Second Mortgage

If you’re interested in obtaining a second mortgage, it’s important to understand the requirements and qualifications needed to secure one. Here are some factors lenders consider when evaluating your eligibility for a second mortgage:

Credit score requirements

Your credit score is one of the most important factors that lenders consider when deciding whether to approve you for a second mortgage. A good credit score, typically above 620, demonstrates to lenders that you are a responsible borrower and able to meet your financial obligations. Now, if you have a lower credit score and a second mortgage doesn’t make financial sense for you, there are other options.

Debt-to-income ratio

Lenders consider your debt-to-income ratio, which assesses the proportion of your monthly income that goes towards debt payments. Ideally, lenders want to see a low debt-to-income ratio, typically below 43%. A high ratio may indicate that you have too much debt and may have trouble making additional mortgage payments.

Equity in home

When you apply for a second mortgage, the equity you have in your home is also taken into consideration. Lenders typically require a certain amount of equity in your home before they will approve you for a second mortgage. The amount of equity required varies depending on the lender and your individual financial situation.

In order to qualify for a second mortgage, you may also need to provide documentation such as income statements or tax returns. It’s important to do your research, compare lenders and their requirements, and ensure that you can meet the qualifications before applying for a second mortgage.

Steps to Get a Second Mortgage

Are you considering a second mortgage? Before you apply, it’s important to understand the requirements and qualifications needed to secure one. Lenders look at several factors to evaluate your eligibility for a second mortgage, including credit score, debt-to-income ratio, and equity in your home. Here are some steps you can take to improve your chances of obtaining a second mortgage.

Preparation and research

Start by preparing your financial documents such as income statements, tax returns, and credit report. It’s essential to review your credit report and address any errors or delinquencies before applying for a second mortgage. Research lenders and compare their requirements, interest rates, and fees. Understand the risks and benefits of obtaining a second mortgage before making a final decision.

Shopping around for lenders

Once you are prepared, it’s time to shop around for a lender that fits your needs. Contact several lenders and ask for detailed quotes, including interest rates, closing costs, and other fees. Provide each lender with the same financial information, such as credit score and income, to ensure fair comparison. Be wary of lenders that request upfront fees or pressure you into borrowing more than you need.

Finalizing the loan

After comparing lenders and selecting one, you can move forward with finalizing the loan. The lender will evaluate the value of your home and the amount of equity you have before approving your loan. Be sure to read and understand all terms and conditions of the loan before signing the agreement. Once the loan is approved, you will receive the funds, and you can use them for any purpose.

In summary, obtaining a second mortgage requires preparation, research, and careful consideration. By understanding lender requirements and shopping around for the best offer, you can improve your chances of obtaining a second mortgage that meets your financial needs.

Finalizing the loan

After comparing lenders and selecting one, move forward with finalizing the loan. The lender evaluates home value and amount of equity before approving the loan. Make sure to thoroughly read and understand all terms and conditions of the loan before signing the agreement. Once approved, receive funds that can be used for any purpose.

Advantages and disadvantages of second mortgages

Second mortgages can offer advantages such as lower interest rates and the possibility of using funds for large expenses like home improvements. However, they also come with the risk of losing one’s home if unable to repay the loan. Additionally, some lenders may charge high fees making the loan more expensive in the long run.

Final Thoughts on How a Second Mortgage Works

Now that you know what a second mortgage is — remember that getting a second mortgage requires preparation, research, and careful consideration. Understand lender requirements and shop around for the best offer to increase the chances of obtaining a second mortgage that meets financial needs. Keep in mind the risks and benefits associated with second mortgages and weigh them accordingly before making a final decision.

If you’re looking for home financing options, Hard Money Lenders has got you covered. We’ve got second mortgage loans in Florida, all you have to do is click here for more information or give us a call at (786) 475-7691.

Yuval Elkeslasi is a distinguished professional in the finance industry, celebrated for his pioneering strategies and significant contributions as the leader of Hard Money Lenders IO. Hailing from Queens, New York, Yuval has built an impressive career, transforming the lending landscape through his expertise and visionary approach. Yuval Elkeslasi

attended Florida State University, where he obtained a bachelor’s degree in Finance. This academic foundation provided him with the necessary skills and knowledge to thrive in the competitive financial arena. Yuval’s tenure at Hard Money Lenders IO is marked by numerous pioneering accomplishments. He has introduced a variety of loan programs designed to cater to specific client requirements, including fix and flip loans, new construction financing, cash-out refinancing, rental property loans, and specialized financing for luxury items like yachts. Among Yuval’s significant achievements is securing an $8 million construction loan for a spec home builder in Port Royal, Naples. He also orchestrated the financing for a prestigious 72’ 2024 Viking Convertible yacht valued at $7.2 million. These transactions demonstrate Yuval’s adeptness at navigating complex financial landscapes and delivering exceptional results.