Blog

Buying Foreclosure Properties with Hard Money

Here at Hard Money Lenders, we’re constantly providing education and unique tips on tapping into the real estate market. Below, our team created The Beginner’s Guide to Buying Foreclosure Properties with Hard Money Loans. The guide gives an in-depth look into the intricacies of leveraging hard money loans for foreclosure properties, paving the way for successful ventures in this lucrative investment niche.

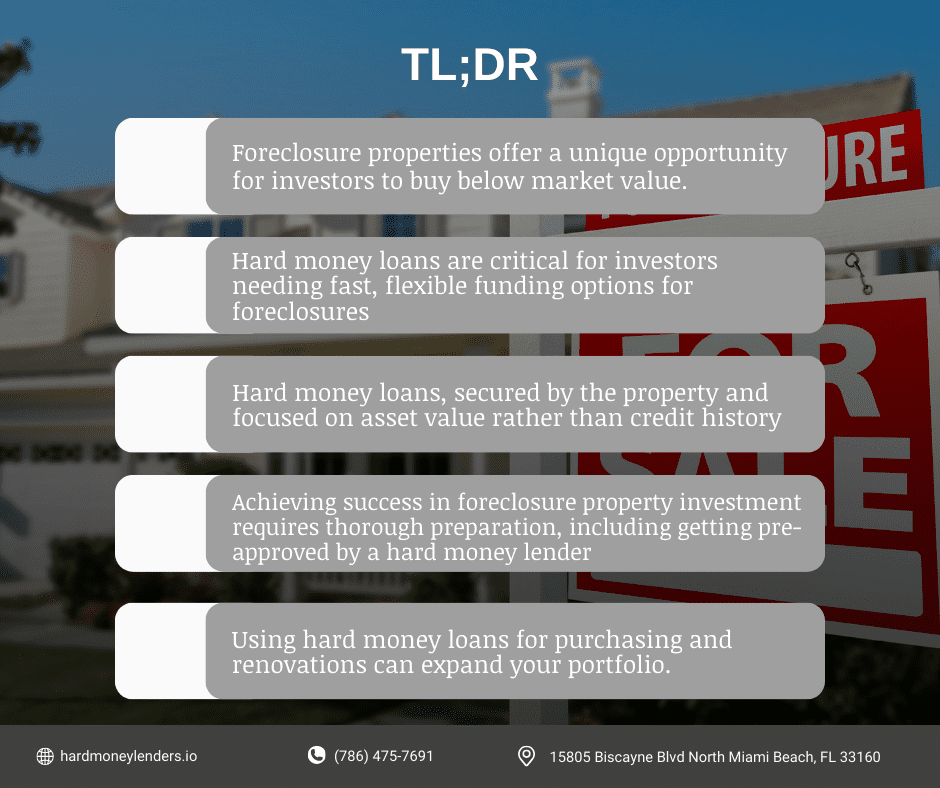

Buying a property for a fix and flip can be more difficult than it seems, as you ideally want to buy a property that needs work but also get it at a low cost. Now, investing in foreclosure properties presents a unique opportunity for real estate enthusiasts looking to expand their portfolio and capitalize on the market’s potential for high returns.

These properties, often available at prices below market value, offer an attractive entry point for investors. However, the challenge frequently lies in securing financing, as traditional lenders typically shy away from foreclosure deals due to the perceived risks involved. This is where hard money loans come into play, offering a solution that aligns perfectly with the swift pace and flexibility required in foreclosure investments.

Before we go over the details about buying foreclosure properties with hard money loans, it’s important to have a clear understanding of foreclosure properties.

Understanding Foreclosure Properties

Foreclosure properties emerge when homeowners default on their mortgage payments, leading banks or lenders to repossess and sell the property to recover the outstanding debt.

This process often culminates in an auction setting where the property is sold to the highest bidder. Foreclosures offer a unique opportunity for investors and homebuyers alike to purchase properties at prices that are typically below their market value, often making them attractive investments.

The Investment Appeal of Foreclosure Properties

The allure of foreclosure properties for investors lies in several key factors. Firstly, their lower purchase price compared to standard market listings can result in significant cost savings upfront.

Additionally, these properties often hold the potential for considerable value appreciation following strategic renovations and upgrades. This aspect is particularly appealing to investors looking to flip the property for a profit.

Furthermore, the process of buying, renovating, and either selling or renting out foreclosure properties can be expedited, allowing for quicker returns on investment. These factors combined make foreclosure properties a potentially lucrative venture for those willing to navigate the complexities of the foreclosure market.

Navigating the Risks of Foreclosure Investments

While the benefits of investing in foreclosure properties are clear, it’s important to acknowledge and understand the risks involved. One of the primary challenges is the legal and financial entanglements that can accompany foreclosure properties.

For instance, there might be unresolved liens, disputed property titles, or issues with the property’s condition that are not immediately apparent. Additionally, the costs associated with necessary repairs or renovations can be substantial, potentially affecting the overall profitability of the investment.

The competitive nature of auctions and the bidding process can also drive up the purchase price, reducing the margin for profit. Successful investors in the foreclosure market are those who conduct comprehensive research and due diligence, carefully assessing each property’s potential risks and rewards before committing to a purchase.

This approach involves evaluating the property’s condition, understanding any legal issues, and accurately estimating the cost and scope of renovations needed to make the investment viable.

How Do I Get Financing for a Foreclosure Auction?

When it comes to auctions for either short sales or foreclosure properties, time is of the essence, so you need to have large amounts of cash on hand. If you have the funds personally to obtain this much cash from your own accounts, that’s great.

However, most people don’t have access to that much cash. Another option is to find an investor who will give you the cash to buy the property. Unfortunately, investors can be hard to find, particularly considering some of the risks associated with buying foreclosure properties, such as the potential costs of evictions or liens.

A final option to consider when it comes to real estate auction financing is hard money loans for auction.

Hard money lenders can get you relatively large amounts of cash quickly and help you successfully bid on a property at auction. For a hard money loan for auction, the property acts as most of the collateral to secure the loan, in addition to a deposit and potentially some other form of collateral.

Hard money lenders require this collateral due to the risky nature of renovating and reselling foreclosure properties, to avoid losing money if something goes wrong.

“Hard money loans for auction can get you large amounts of cash quickly and help you successfully bid on a property at auction.”

Should I Use Hard Money Loans for an Auction?

Hard money loans are a great way to buy foreclosure properties if you plan to fix and flip the property or use the “BRRRR” (buy, rehab, rent, refinance, repeat) method of investing in real estate. If you’re located in Florida and interested in the BRRRR strategy, consider a rental property loan! In these situations, hard money loans can be a great way to finance your goals and turn a profit.

However, if you are buying a foreclosure property because you plan to live there, a traditional hard money loan may not be your ideal method of funding.

Hard money loans are usually short-term and aren’t designed for occupying a house or property. If you’re looking for financing to buy a home or property to live in, consider a bridge loan instead, which will help you get fast funding to buy a property while you look for a mortgage.

Keep in mind that none of this is financial advice, and it’s important to conduct due diligence before taking out a loan.

The Basics of Hard Money Loans

Hard money loans are a helpful financing tool in the real estate investment realm, particularly suitable for transactions like foreclosure purchases that require swift action.

These loans are extended by private investors or companies, and their security is primarily based on the real estate asset being purchased rather than the borrower’s credit history or income.

One of the defining features of hard money loans is their rapid approval process, which can be crucial for investors looking to capitalize on time-sensitive opportunities in the foreclosure market.

The flexibility of terms, including loan duration, repayment schedule, and interest rates, further adds to their appeal, allowing for tailored financial solutions that accommodate the unique needs of each investment project.

Leveraging Hard Money for Foreclosure Investments

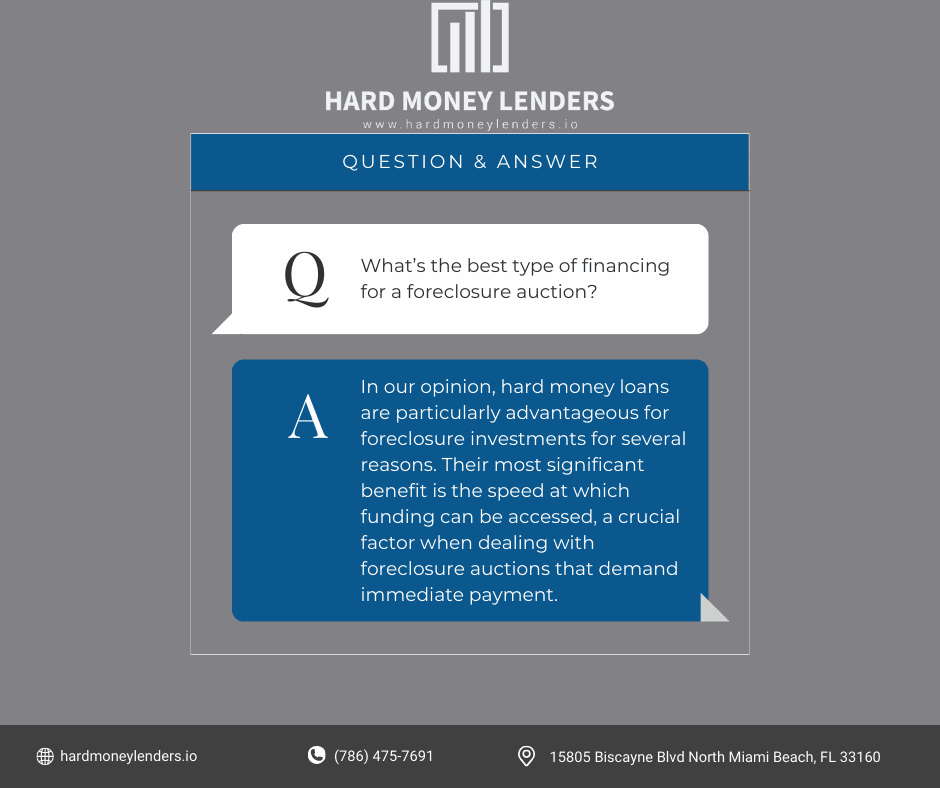

Hard money loans are particularly advantageous for foreclosure investments for several reasons. Their most significant benefit is the speed at which funding can be accessed, a crucial factor when dealing with foreclosure auctions that demand immediate payment.

This swift funding ensures that investors can compete effectively in the fast-paced foreclosure market, securing properties that would otherwise be beyond reach due to the time constraints of traditional financing methods.

Another critical aspect of hard money loans is their focus on the asset’s value rather than the borrower’s financial history. This criterion widens the pool of potential investors, especially those who may have solid investment strategies but are held back by less-than-perfect credit scores or unconventional income sources.

By assessing the investment based on the property’s value and the proposed renovation or flipping plan, hard money lenders align their interests with those of the investor, focusing on the potential return on investment rather than traditional lending criteria.

This approach to financing is particularly suited to the nature of foreclosure investments, where the property in question may require significant renovation before it can realize its full market potential.

Hard money loans provide the necessary capital to not only purchase these properties but also cover the costs of renovation, allowing investors to transform undervalued assets into profitable ventures. The inherent flexibility and rapid deployment of funds make hard money an indispensable tool for investors aiming to leverage the opportunities presented by foreclosure properties.

How Do I Buy a Foreclosure Property With Hard Money Loans?

If you are seriously looking to buy a foreclosure property, you need to be prepared to have cash on hand for the auction. Hard money loans are a great way to quickly get access to the cash you will need. It’s important to get pre-approved by a hard money lender before you bid on a foreclosure property at auction, so that you won’t have to wait to get financing if you win the real estate auction.

As part of this process, you will need to give your hard money lender information ahead of time such as what property you plan to bid on, the expected ARV (after-repair value), a research report on the title indicating what liens or liabilities are on the property, and the maximum bid that you plan to pay for the property.

This is all in addition to any other necessary loan documentation (such as your exit strategy), your deposit, and any other collateral required to obtain the loan. Using this information, the hard money lender will decide how much of your maximum bid they are willing to finance. If you are bidding on multiple properties, you will have to provide this information to your hard money lender for each of them.

Bidding on A Property After Getting Pre-Approved

“It’s important to get pre-approved by a hard money lender before you bid on a foreclosure property at auction.”

After you’ve been pre-approved for the loan, you’re ready to place a bid on a property at auction. If you win the foreclosure auction, the loan can become official very quickly, releasing the necessary funds to you so that you can pay the auction company and certify your purchase.

If you find a suitable hard money lender before trying to make a short sale or attending a foreclosure auction, hard money loans can be a great way to get real estate auction financing. Hard money loans for auction will allow you to place bids at a foreclosure auction confidently and get funding fast if you have a winning bid.

To learn more, check out our guide to “Using Hard Money for Properties at Auction.”

Advanced Strategies & Tips for Foreclosure Investment Success

Leveraging Hard Money Beyond Purchasing

Smart investors recognize that the utility of hard money extends far beyond the initial acquisition of foreclosure properties. By using these funds for both buying and renovating properties, investors can significantly accelerate the investment cycle, from purchase to sale or rental. This strategy not only optimizes the use of hard money loans but also enhances the property’s market value and appeal at a faster rate, allowing for quicker turnovers and increased profitability.

To effectively implement this approach, investors should:

- Plan Comprehensive Budgets: Develop detailed budgets that encompass both acquisition and renovation costs, ensuring that the hard money loan covers all aspects of the investment.

- Select Value-Adding Renovations: Focus on renovations that significantly increase property value, such as kitchen and bathroom remodels, while avoiding unnecessary upgrades that do not offer a strong return on investment.

- Streamline Renovation Processes: Establish relationships with reliable contractors and suppliers to ensure renovations are completed efficiently and within budget. Time is money, especially when interest on hard money loans is considered.

By adopting a holistic approach to using hard money, investors can reduce holding times and interest expenses, thereby maximizing the potential returns from their foreclosure investments.

Building Your Investment Portfolio

Expanding a portfolio of foreclosure properties requires a deliberate and strategic approach, with an emphasis on diversification and long-term growth.

A diversified portfolio reduces risk by spreading investments across different property types, locations, and investment strategies (such as flipping and renting). This approach helps mitigate potential losses in one area with gains in another, leading to more stable overall returns.

Strategies for portfolio expansion include:

- Market Research: Continuous research into emerging markets and undervalued areas can uncover new opportunities for foreclosure investments.

- Reinvesting Profits: Use the profits from successful flips or rental income to fund additional purchases, creating a self-sustaining growth cycle for your portfolio.

- Networking: Building relationships with other investors, real estate professionals, and hard money lenders can provide insights and opportunities that are not available through traditional channels.

A focused strategy on portfolio development ensures steady growth, minimizing risks and maximizing returns over time.

Risk Management and Mitigation

Effective risk management is the cornerstone of sustained success in foreclosure investment. This involves not only diversifying your investment portfolio but also conducting exhaustive due diligence on potential properties and maintaining a financial buffer to handle unforeseen expenses.

Key aspects of risk management include:

- Thorough Due Diligence: Before purchasing a property, conduct in-depth research to uncover any legal issues, structural problems, or financial encumbrances that could affect the investment’s profitability.

- Financial Reserves: Maintain a reserve fund to cover unexpected costs, such as emergency repairs, prolonged vacancies, or market downturns. This financial cushion can prevent the need for distress sales and allow for strategic decision-making.

- Continuous Education: Stay informed about market trends, legal changes, and new investment strategies. An informed investor is better equipped to anticipate risks and adapt strategies accordingly.

By implementing these advanced strategies and maintaining a focus on risk management, investors can navigate the complexities of the foreclosure market more effectively, leading to greater success and profitability in their investment endeavors.

Final Thoughts

Investing in foreclosure properties with hard money loans can offer a pathway to significant returns for those willing to navigate the complexities of this investment strategy. By understanding the process, from identifying potential properties to securing the right financing and executing a well-planned renovation and exit strategy, investors can unlock the true potential of foreclosure investments. With the right approach, foreclosures can become a valuable addition to any real estate investment portfolio, offering opportunities for growth and profitability in the ever-evolving property market.

Frequently Asked Questions (FAQs) About Hard Money Loans & Foreclosures

How do I find foreclosure properties?

There are many websites that can help you find foreclosure properties coming onto the market, such as Auction.com and Foreclosure.com (See related article: 13 House Flipping Apps to Make Your Fix and Flip Easier). You can also consider reaching out to local real estate agents who may have local knowledge.

What’s the difference between buying a foreclosure short-sale and at auction?

Short Sale

Technically, selling a property short-sale means selling it pre-foreclosure. The borrower that owns the property has stopped paying the bank, perhaps due to situations like bankruptcy or even death, and so the bank is trying to avoid losing out on the money they loaned.

Foreclosures typically result in a major financial loss for the bank, even if the property is sold at auction.

Once the bank legally initiates official foreclosure proceedings, investors can offer the bank and current owner a sum and try to buy the property for a good price. This is called a short sale. The key to buying a property in this way is to offer less than the market value of the property, but make sure that your offer is still more than what the property’s worth to the bank will be after the loss due to foreclosure.

The bank and property owner will usually be relieved to avoid foreclosure, and you can get a good deal on a property.

If you have the option to buy a property pre-foreclosure with hard money loans, doing so is usually preferable to trying to buy a property at an auction.

This is because you can inspect the property before purchase and evaluate the necessary repairs, as well as not having to deal with the extra costs that can come with auctions.

Foreclosure Auction

Unlike short sales, foreclosure auctions take place after formal foreclosure proceedings have already happened. This mainly occurs if the bank is unable to get rid of the property in a short sale, at which point they will try to sell the property at an official auction.

Foreclosure auctions can be unpredictable and competitive, with a wide variety of potential buyers, many of whom may be experienced real estate investors. Properties must usually be paid for with a down payment (usually of at least 10%) immediately after winning the auction and paid in full within a day.

What happens if I can’t pay back the loan?

Ideally, after using a hard money loan to purchase a foreclosure property at auction, you will renovate the property and either sell it for a profit or rent it and refinance your loan, as we have described above. However, if you’re unable to pay back the loan in full, hard money lenders will take your collateral to make up for it and then sell off the property to pay off the remainder of the debt. Hard money lenders accept a good deal of risk when they offer loans to buy foreclosure properties, and to continue doing so they must act quickly to make up their loss when a borrower defaults on the loan.

I won a bid on a foreclosure property at auction. Now what?

Once you have successfully won a bid and paid your deposit, you can sort out the contract.

Most hard money lenders will want you to open a new LLC for this, rather than having the contract be made out to you personally. This is important for investors in real estate because it won’t affect your personal credit score and involves less liability for you and less paperwork.

After you send the contract the court and close within 30 days, you should get an appraisal and title search, to check for liens and liabilities on the property. To ensure your appraisal is accurate and you get a legitimate ARV, hire a contractor and plan out the work that will be done.

Once you have these numbers, you can close the deal and begin renovations. You will need to borrow funds for renovations in draws and provide part of the money yourself for each draw.

Finally, once renovations are completed, it’s time to make a profit! You can either rent the property out and refinance a loan on it with a traditional bank or put the property on the market and sell it. Once your property sells successfully, your hard money lender should receive funds from whoever is providing a mortgage for your buyer. This should effectively pay back your hard money loan. Your profits will be released to you!

Yuval Elkeslasi is a distinguished professional in the finance industry, celebrated for his pioneering strategies and significant contributions as the leader of Hard Money Lenders IO. Hailing from Queens, New York, Yuval has built an impressive career, transforming the lending landscape through his expertise and visionary approach. Yuval Elkeslasi

attended Florida State University, where he obtained a bachelor’s degree in Finance. This academic foundation provided him with the necessary skills and knowledge to thrive in the competitive financial arena. Yuval’s tenure at Hard Money Lenders IO is marked by numerous pioneering accomplishments. He has introduced a variety of loan programs designed to cater to specific client requirements, including fix and flip loans, new construction financing, cash-out refinancing, rental property loans, and specialized financing for luxury items like yachts. Among Yuval’s significant achievements is securing an $8 million construction loan for a spec home builder in Port Royal, Naples. He also orchestrated the financing for a prestigious 72’ 2024 Viking Convertible yacht valued at $7.2 million. These transactions demonstrate Yuval’s adeptness at navigating complex financial landscapes and delivering exceptional results.